Outlook for global construction equipment markets: China

First published in Global Report: Construction Equipment 2016 as Will earthmovers become the global growth champions?

Sinoma Anhui cement mine in Anhui Province

Sinoma Anhui cement mine in Anhui ProvinceA Freedonia Group report published in July 2015 says that Chinese construction expenditure will grow 7.8% annually until 2019, fuelled by an increasing urban population, continued industrialisation, expanding foreign investment and rising personal income levels

In addition, the government’s effort to sustain growth in the manufacturing sector, improve the country’s infrastructure, expand municipal utilities, and balance regional economic disparity will, says Freedonia, help growth in construction spending. However, further growth will be restricted by a slowdown in the Chinese economy, especially in fixed asset investment.

China consists of several regional markets characterised by different climates, populations, and levels of economic development. According to Freedonia, the Central-East accounted for 43% of the annual average 17.6 trillion yuan (US$2.75 trillion) construction spending in China in 2014, higher than its share of population or economic output. However, Freedonia says the region will see slower growth until 2019 than the other five regions of China – 7.2% a year – mainly due to the large size of its existing stock. Construction expenditures in the Northwest are forecast to rise 9% yearly in real terms through 2019, outpacing all other regions. Freedonia tips China’s Great Western Development strategy to result in sizeable gains in spending on infrastructure and manufacturing applications in this region.

Despite Freedonia’s forecast of rising construction expenditure, a senior executive from Caterpillar, the world’s biggest selling OEM, says he does not expect Chinese demand for excavators to recover to the peaks of 2010-12.

Tom Pellette, Caterpillar group president for construction industry equipment, made his prediction to the UK’s Financial Times newspaper in November 2015 after the Chinese economy recorded its slowest growth rate since 2009 in the third quarter, due to declining construction and factory activity, which many economists do not believe has bottomed out yet.

Pellette said industry-wide sales of 10-90tonne hydraulic excavators will reach the “23,000 range” in China this year. That compares with a total of more than 27,000 sold in March alone in 2011 and more than 112,000 for the whole of 2010, which was the peak year for the market. The company does not disclose figures for sales of its own products by country.

“That shows how far off the peak we are,” Pellette told the Financial Times. “My expectation is within China and globally that the market will pick up to a level above where we are in 2015. But for China specifically, our expectation is that the market will rebound but we are not planning [for it to] get back to 2011/2012 levels.”

Global Market data

Global Market dataDespite the immediate headwinds, Pellette is optimistic about the long-term future for the company’s business in the world’s second-largest economy in part because the urbanisation of the country has some way to go. Caterpillar also cited the government’s plan to double both the gross domestic product and income base between 2010 and 2020.

Others are voicing concern over the state of the Chinese construction equipment market over the coming years.

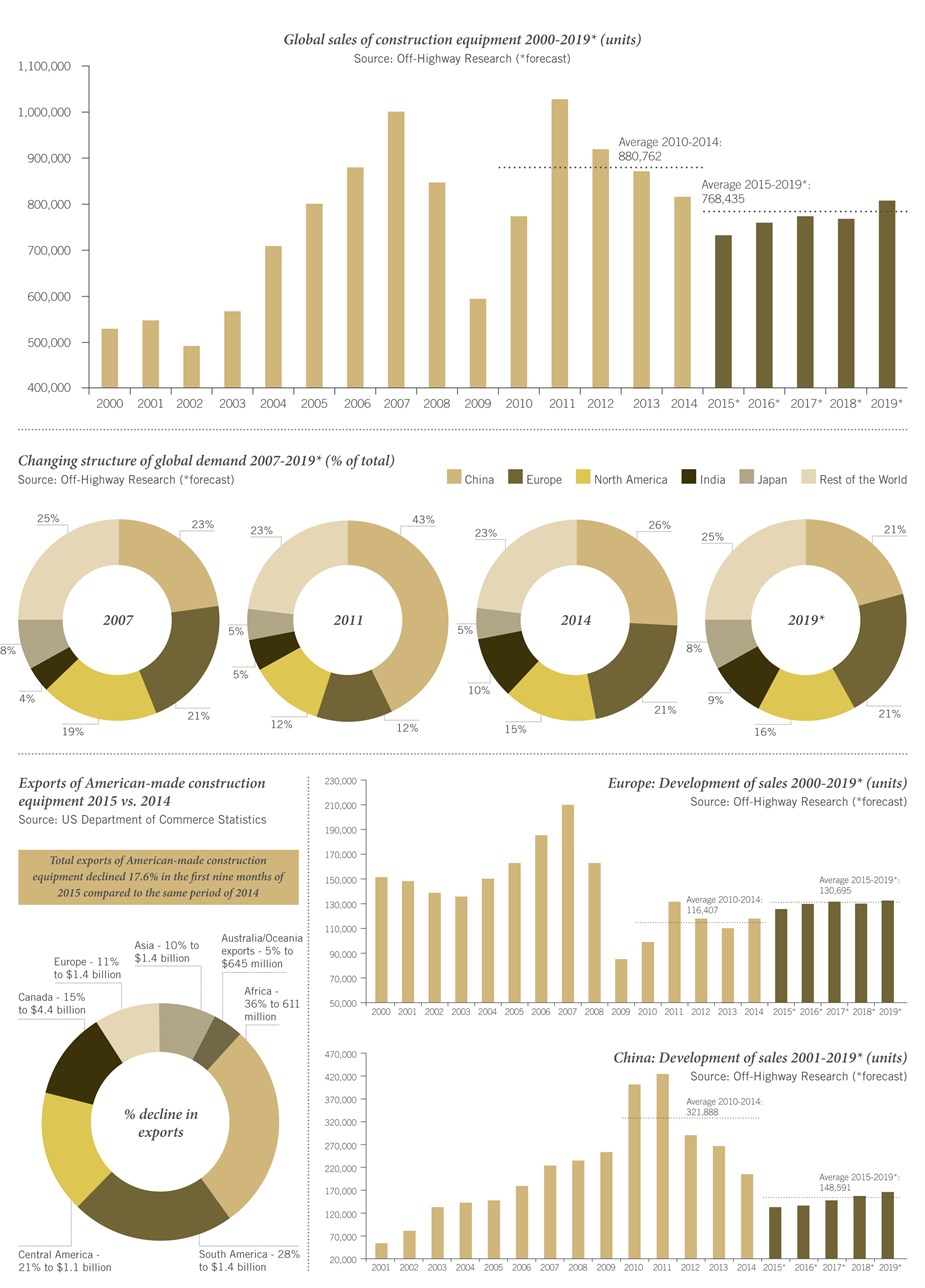

In a speech at a LiuGong event in June 2015, David Phillips, managing director of Off Highway Research (OHR), a management consultancy specialising in the research and analysis of international construction and agricultural equipment markets, said annual average Chinese construction equipment sales for the period 2015-19 are forecasted to fall to 160,021 – almost half the 319,399 sales posted in the years 2010-14.

Within the overall figures, Phillips said OHR was expecting wheeled loader sales to drop to an annual average of 64,000 from 2015-19, compared to 162,782 in the period 2010-14. Crawler excavator sales are also, said Phillips, set to average 58,800 a year for the years 2015-19, compared to 113,244 in the period 2010-14.

Among key challenges facing Chinese construction-based OEMs, said Phillips, was the need to reduce production overcapacity by 50%. OHR’s latest figures show the annual average of units produced in the years 2010-14 at 356,793, compared to 225,153 units over the 2005-9 period.

Companies in this article

Caterpillar

LiuGong

Freedonia Group