Outlook for global construction equipment markets: Africa

First published in Global Report: Construction Equipment 2016 as Will earthmovers become the global growth champions?

A Volvo CE excavator loads a tipper truck at a quarry in the Mpumalanga province of South Africa

A Volvo CE excavator loads a tipper truck at a quarry in the Mpumalanga province of South AfricaThe African construction equipment market may offer huge potential growth, but that seems a long way off at present. An example of this can be found in new ISC figures showing a 25% drop in Africa earthmoving equipment sales in H1 2015, compared to the same period of 2014

Something needs to be done to address Africa’s perennial growth restrictors: corruption, weak currencies, red tape and lack of quality road and other logistics infrastructure.

On a more positive note, many leading figures among globally renowned OEMs are still optimistic about the African construction equipment market – including Andy Blandford, CNH Industrial Construction Equipment Vice President Europe, Africa and Middle East.

In a recent interview with Aggregates Business International, Blandford said African quarrying and heavy construction customers are, like their counterparts in Europe and the Middle East, now beginning a steady process of fleet renewal with a big focus on total cost of ownership (TCO).

“Africa is an industry of around 23,000-25,000 units, and although the continent is absolutely huge, we have to [primarily] focus, to be successful, on sub-Saharan Africa. The biggest market within that is South Africa at about 6,000 units. We have an office in South Africa with a number of people there, as we believe we need people locally in the market in order to be successful.

“The second focus for us is in Africa is the Maghreb region: Algeria, Tunisia, and Morocco, in that order, as the second biggest Africa market is Algeria. The market there is today giving us and our competitors some difficulty. Due to the availability of currency, there are some import restrictions in place. The restrictions, though, will come off.

“The African market on a 12-months’ rolling basis is down about 7-8%. It doesn’t look that great today, but you have to say that if you look at Case globally, one of the largest growth opportunities we have is Africa. The question is when that growth will happen. The answer is different for all countries within Africa. It depends on things such as infrastructure investment and availability of capital.”

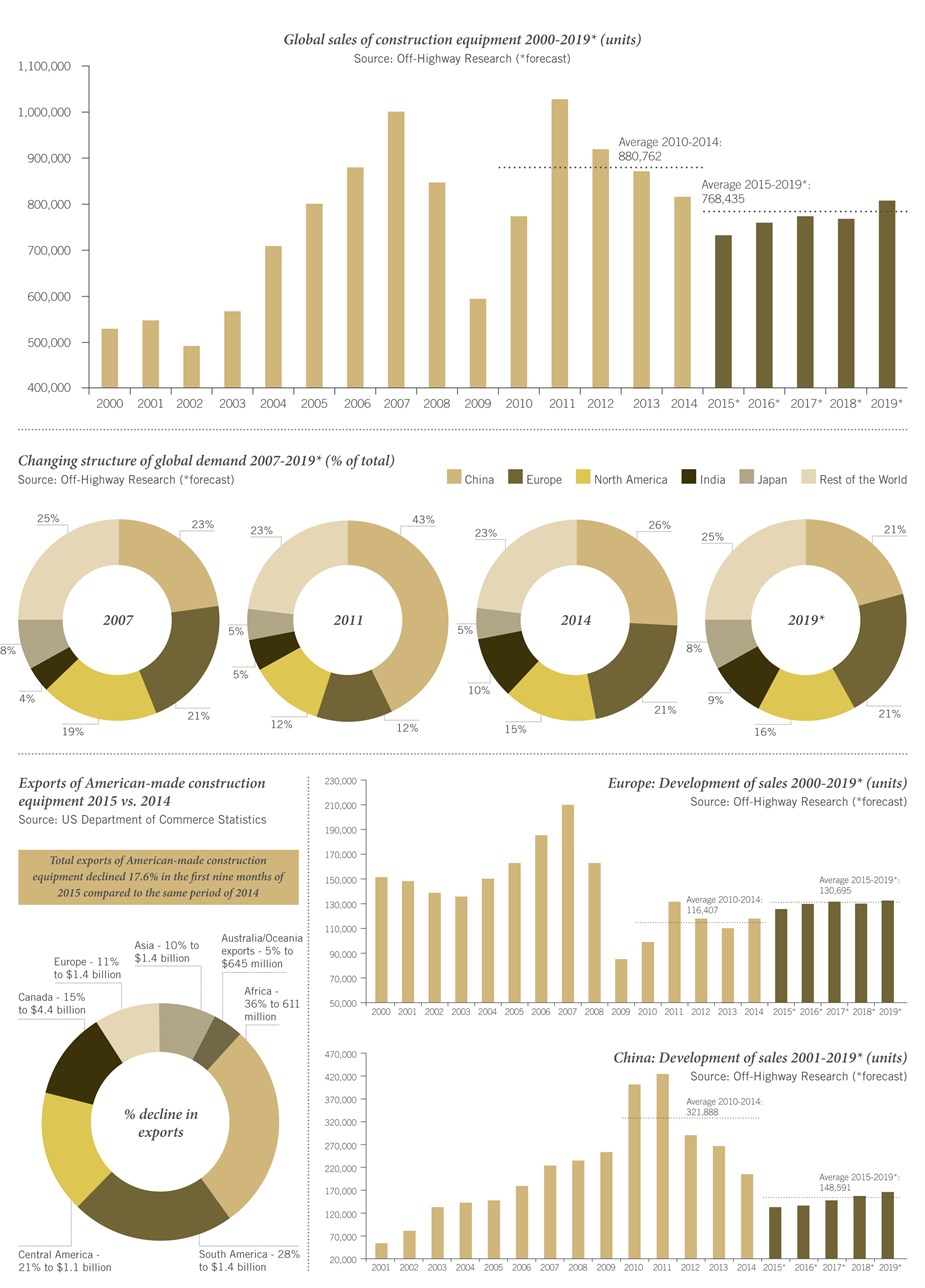

Global Market data

Global Market dataAccording to a recent Timetric report, the South African construction industry is set to benefit from the national government’s adoption of the National Infrastructure Plan (NIP), with accompanying National Budget estimates in order to develop South Africa’s infrastructure. The proposed large number of announced projects provide hope for a construction industry which is, as Timetric notes, hindered by corruption, mismanagement and price fixing, all of which threaten to undermine the proper implementation of the NIP. Nevertheless, Timetric expects the South African construction industry to record a CAGR of 8.93% over the forecast period (2014–2018).

As Munesu Shoko reported in a recent edition of ABI, West Africa is the second biggest region as far as investment into infrastructure development is concerned – creating huge sales opportunities for construction-based OEMs. Total value of projects under construction increased from US$50 billion in 2013 to US$75 billion in 2014. Although the region only accounts for just half of Southern Africa’s spend, it is starting to close its infrastructure gap, anchored by Nigeria with its new title as the biggest economy in Africa.

With a large population of 170 million people, coupled with a rebased economy that now stands at the helm of African economies, Nigeria is a hot spot for the building and construction materials value chain at large. Its construction growth will be the fastest of all global markets by 2018, according to Global Construction Perspectives’ Global Construction 2020 report. It says Nigeria is the “global hotspot from here to 2020” and its construction growth will even be faster than that of India.

East Africa has about $67 billion worth of construction projects under way. It is historically among Africa’s least developed regions, but with ongoing infrastructure development, coupled with several member countries boasting higher GDPs, the region has transformed into a strategic hub for aggregate producers, and, as such, an attractive growth region in which to sell construction equipment. With countries such as Ethiopia (9.5% in 2015) and Rwanda (7% in 2015) relishing higher GDPs, Kenya’s infrastructure development projects firing from all cylinders and Tanzania’s oil and gas finds turning the heads of investors, East Africa is well and truly on the up.